.png)

Whilst not ignoring the euphoria around stablecoins for P2P, democratising USD access and yield within the investment portfolio of Fabric Ventures, I had quietly been looking in 2024 for a team tackling the much larger TAM of B2B payments by leveraging stablecoins. It was also key for me to find a team who understood that the payment part of B2B is just the visible tip of the iceberg and there is much more to solve than this relating to the broader billing systems that merchants are so dependent on.

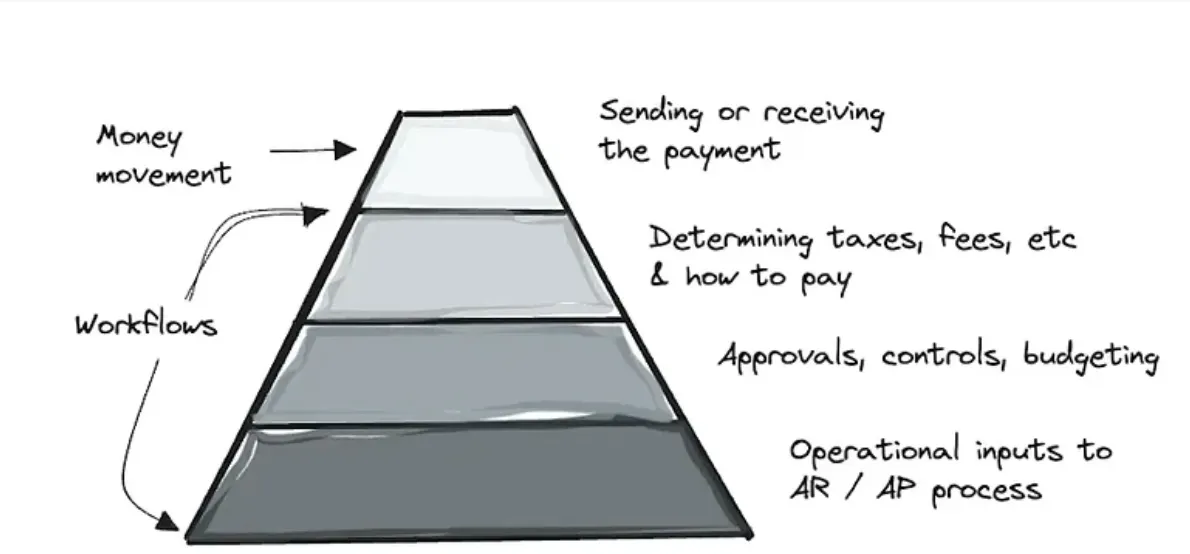

The Complexity Behind B2B Payments

Matt Brown’s piece covers this additional complexity for B2B payments in general. Illustrated by the pyramid below:

I quote from his piece:

“…What’s hardest, most broken, and ultimately most valuable in B2B payments? The workflows and data that are the precursor to the payment being made.”

Early Experience in Billing Systems

2001 — Telecom Industry Shift

Back in 2001, whilst at Bear Stearns, I was introduced to the complexities of billing systems, advising Geneva Technologies on its $700m sale to Convergys in the telecom industry. Accepting money for the customer payment was the simple part.

Operators were suddenly required to have a unified and convergent view of customers covering their Internet, telecoms, and cable TV usage. Billing systems did this work as well as integrating to existing providers’ infrastructure, such as:

- Finance and accounting

- Customer relationship management systems

Mediation systems - Other rating systems

2010–2015 — SaaS Billing Transformation

Roll forward some 10–15 years during the 2010–2015 period, and I witnessed similar dynamics in billing systems upheaval. This time within the context of B2B e-commerce.

During my days at PayPal we partnered with companies such as Recurly (now KKR owned) and Chargebee. Both successfully rode the growth wave of SaaS customers.

At the time, SaaS businesses had to either build their own in-house billing system or rely on clunky enterprise tools that weren’t designed for SaaS models. These teams understood that SaaS presented new challenges in billing and payments including addressing failed payments and reducing involuntary churn (failed payments due to expired cards, insufficient funds, or technical errors). The latter being one of the most significant issues for subscription businesses. This silent source of revenue drain can account for up to 40% of churn.

Billing systems also had to deal with managing much more complex flows such as tiered pricing, usage-based models, and mid-cycle plan adjustments and of course due to starting with SMBs who adopted SaaS initially, had to scale fast with customer growth.

Today’s Transformation in Merchant Billing

Another 10 years later, we are today witnessing a further transformation in merchant billing. This time it is driven by two tailwinds:

a) First: Growth in merchant stablecoin acceptance.

Initially this comes from blockchain infrastructure providers such as RPC node infrastructure and data analytics companies (serving respectively developers or traders on-chain).

As more and more merchants embrace stablecoins, more of their assets end up sitting in stablecoins and they then themselves become eager to spend them and the flywheel kicks in. This is the playbook that PayPal have within their 2 sided network leveraging PYUSD.

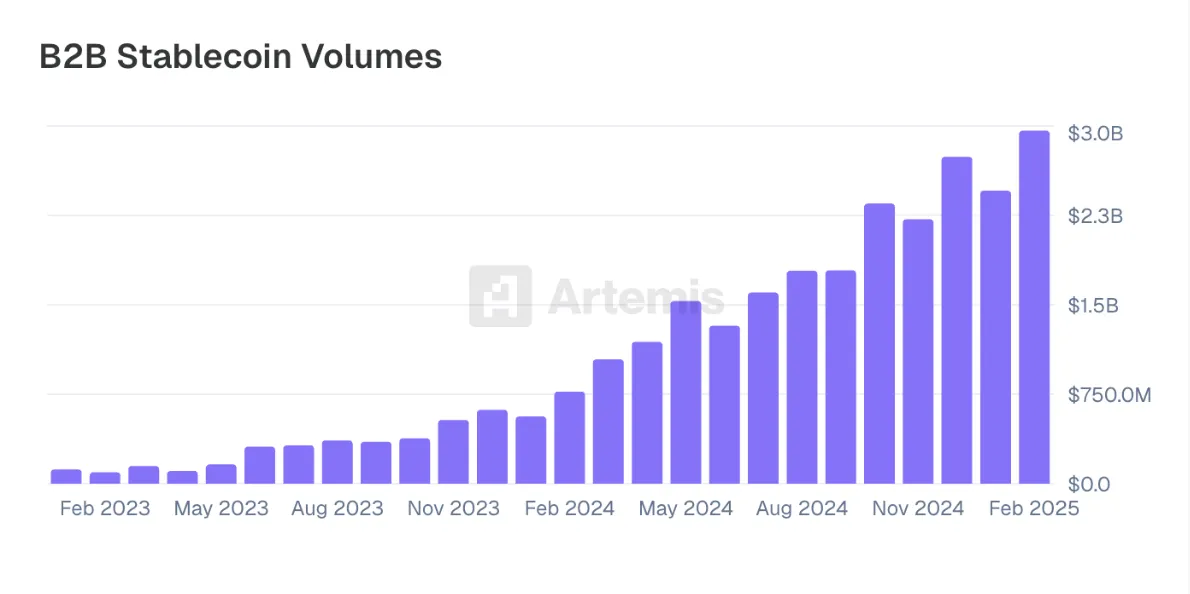

Stablecoin use for B2B has 2x in the period July 2024 to February 2005 to 3bn$ in volume, making it the largest component of payments on-chain at almost 50% according to Artemis. Annual run rate pace for these settlements totalled approximately $72.3 billion in February 2025.

b) Second: Growth in usage based billing most recently driven by AI vendor business models.

Even PayPal is relaunching its own recurring billing platform to address usage based billing for AI business models.

At Fabric we also have a firm belief that these 2 tailwinds will combine forces, in that AI usage based models will increasingly be stablecoin based as well — because these same stablecoins address the challenges in AI/agentic usage models of settlement speed, global demand, autonomous authorisation and microtransaction pricing for say 0.3 seconds of GPU time vs paying for a monthly plan.

LoopCrypto

I was lucky to meet and invest in LoopCrypto. They tap into both of these tailwinds. I first became intrigued by LoopCrypto in August 2024 on the back of Eleni’s (the CEO) blog and then was subsequently invited to join a round at a later date, by our friends at VanEck Ventures:

Eleni had seen the power of stablecoins in helping B2B payments:

The bottom line is that existing B2B payment rails are not well designed for developers in Kenya or Brazil trying to subscribe to AI tools hosted in the U.S. and paying in local currency. This year, companies across the globe are projected to spend over $700B on cloud infrastructure services. Much of this spend will be cross-border.

These global merchants are no different to recipients of cross border P2P payments, they prefer payments that settle faster for vital cashflow and they prefer to offer cheaper solutions to their customers.

In addition, any business which spends meaningful CAC/branding dollars to attract prospective customers, will be very aware that a majority of online shoppers will abandon their carts if they don’t see their preferred payment method. Today that method increasingly includes stablecoins. This is not a small merchant phenomenon; Google Cloud accepts PYUSD as requested by their client, PayPal.

Solving B2B Payment Workflows

Eleni also understood that anyone managing vendor payments in B2B needs to be able to directly or indirectly solve for complex B2B payment related workflows such as:

- Tracking the contract details, item sold, or usage amount to derive the amount to be paid

- Validating that the payment amount sent equals the amount due

- Collecting the required regulatory info

- Calculating and withholding the correct taxes

- Ingesting and reconciling the contract, invoice, and payment with internal tools like CRMs, revenue insights tools, and financial reporting that help businesses run

- Offering custom payment flows that take into account adding sales tax or a tip or a platform managing subscriptions for many contributors, each with their own various payment configurations or conditional payments such as selling APIs and charging when a threshold is hit or selling business software and charging per seat when a new seat is added

Crucially, LoopCrypto works with incumbent billing systems to avoid a rip and replace, and thus minimises additional setup and ongoing maintenance work.

LoopCrypto integrates with the billing tools that merchants already use like Stripe, OpenPay, and Chargebee. This allows merchants to handle fiat and crypto payments via the same platform.

After adding crypto payments, with LoopCrypto in such a unified way, Helius’s crypto payment volume has grown 25% month-over-month.

Wedge Strategy and Traction

Breaking into a market often requires a wedge targeting a niche part. Accepting stables and integrating with strategic billing systems, would likely position the company well but for a slower ramp up over time as merchants gradually added stablecoins.

With an entry wedge solving a particular immediate pain point growth can be significantly expedited.

LoopCrypto’s traction to date has come from riding the wave of usage based models as seen in developer tools, creators, gaming platforms and in particular AI solutions. The subscription economy is worth over $650 billion globally and growing at 435% annually. The global AI software market is forecasted to reach $467 billion by 2030.

LoopCrypto’s wedge has been solving their pain point of accepting the required recurring payments using stablecoins. This is a more challenging task in the push payment model used on-chain.

The Recurring Payment Problem

Before LoopCrypto, recurring payments on-chain equated to locking up funds in a smart contract, managing complicated streams of tokens, or sending repeated emails with payment links.

Without recurring autopay, churn can be 2x higher (adding friction from the renewal process). In addition, merchants see a 15% increase in customer retention when enabling autopay and a delinquency rate of 6% compared to 17% for manual payments as payment information is securely stored and processed automatically when due.

Anywhere from 20–40% of all SaaS churn is involuntary, meaning the customer intended to keep using your product, but the payment method failed so the customer canceled rather than continuing their subscription. In the case of crypto this could be due to a low wallet balance.

As such, recurring billing providers should, such as LoopCrypto does, provide dunning solutions and preferably on an automated basis. A proactive approach to this can reduce merchant fees due to identifiable failures and avoid merchants having their standing with payment processors negatively impacted.

There is much more to come in B2B payments than the above payments technicalities, as solutions become very specific to verticals and payments are hidden within software addressing specific workflows such as payroll, treasury management or escrow solutions. LoopCrypto’s APIs are well positioned to target these vertical solutions as well.

The Contextual Data Play

An exciting direction for growth is for LoopCrypto to enable an open data contextualisation platform which standardises, stores, and makes payment data accessible (a layer similar to the role that Plaid plays in Web2).

In the Web2 world, there would be a card network or a Plaid API that would communicate a merchant category and other payment details via shared communication standards. This is why in Web2 banks and FinTech applications can provide the customer with a rich spend history with context on where money was spent and for what.

On-chain, all we have access to is a block explorer to try to decipher the context around transactions. Instead, we need metadata like an invoice, credit agreement, or bill of sale.

Making this data available powers post-payment opportunities, such as:

- Proving a businesses revenue on-chain to banks, lenders, and governments

- Easily producing financial statements that account for on-chain revenues

- Analysing customer and provider personalisation by looking at the customer’s on-chain history

- Understanding preferred payment chains and tokens

- Identifying high-performing products and services

- Calculating the success of a coupon or marketing campaign

- Powering new financial markets on-chain such via credit scoring

The Consumer Bet

The opportunity on-chain is not just for merchants but there is a bigger consumer bet as well:

On stored payment profiles e.g. Stripe Link or Shop Pay, but for crypto. A one-click checkout experience, portable across merchants but where users actually own their own payment profiles and history on-chain.

After all, the killer feature of Web3 is sovereign ownership and interoperability. Solutions that solve these payment related workflows and empower end users, will be the ones who earn the right to process the payment of the future.

• • • • •

For more information on Fabric’s portfolio, opportunities and our investment thesis please visit our website and follow us on Twitter, LinkedIn, Farcaster & Lens.