.png)

Stablecoins and blockchain payments didn’t emerge overnight. They’re the product of an evolutionary journey.

Since the 2008/9 financial crisis, we’ve been addressing inefficiencies in financial services. Regulatory shifts, digital payments, smartphones, and Bitcoin’s accessibility and store of value paved the way for improvements, led by fintechs. These innovations, as documented by The Motley Fool, have made finance cheaper, safer, and more accessible. Stablecoins and crypto payments are the natural next step in this evolution.

The first wave of blockchain payments brought hype but ended in disillusionment:

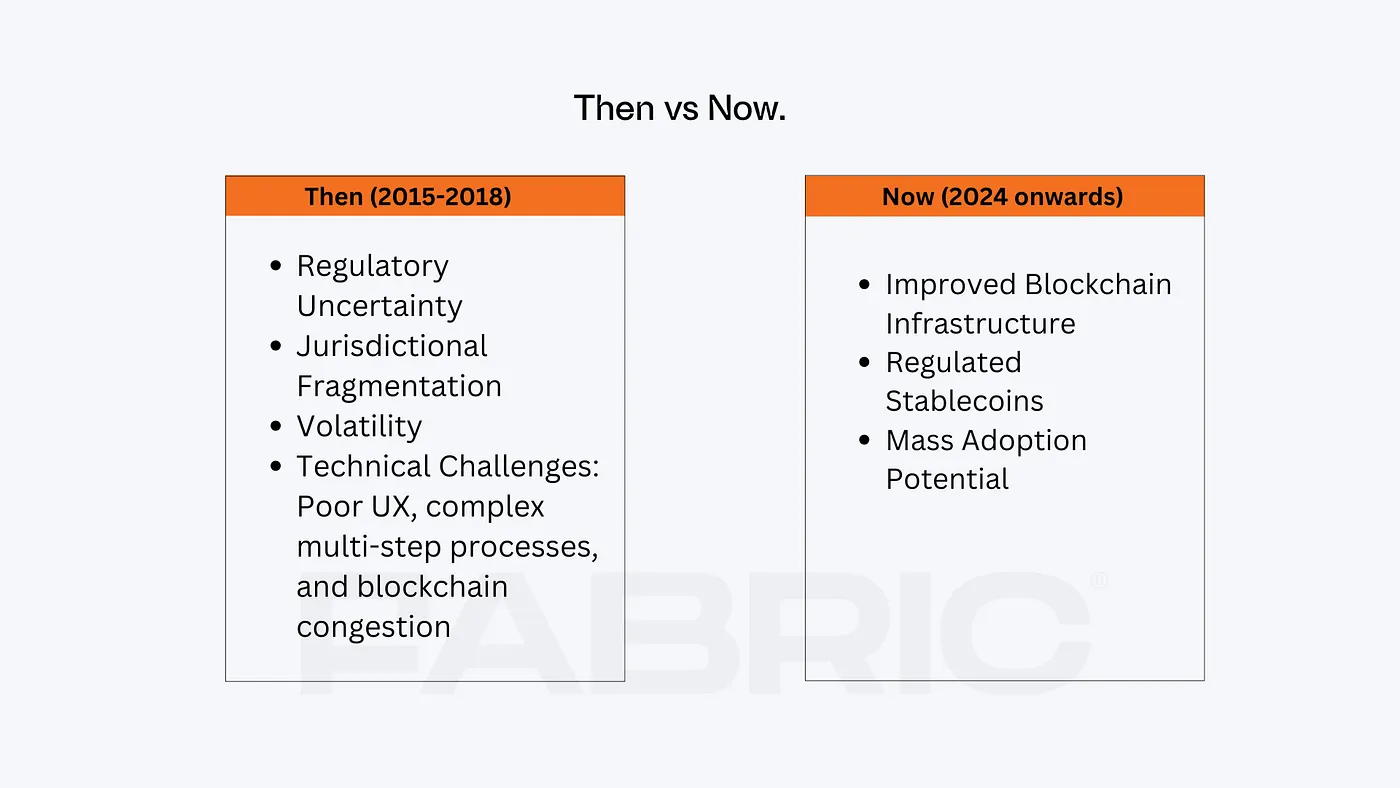

- Regulatory Uncertainty: Is a digital transaction an asset, a commodity, a security, or a currency? Is it taxable?

- Jurisdictional Fragmentation: Different AML regulations across countries created friction.

- Volatility: Crypto price swings made merchants hesitant to accept payments.

- Technical Challenges: Poor UX, complex multi-step processes, and blockchain congestion led to slow speeds and high fees.

Fast forward to now:

- Improved Blockchain Infrastructure: Reliable, scalable, and cost-effective.

- Regulated Stablecoins: Offering trust and liquidity while solving volatility.

- Mass Adoption Potential: Payments remain a $1.9 trillion industry, ripe for disruption (McKinsey).

The current focus on stablecoins reflects a decade of innovation, heavily backed by VC investment. From the early days of Bitcoin payments — where Paxos (an investment by my old alma mater PayPal Ventures) and Circle (a Pantera Capital investment, which we at Fabric backed and collaborated on) emerged — to today’s locally regulated, tokenized fiat currencies, stablecoins have matured alongside API-driven Banking as a Service (BaaS) and Payments as a Service (PaaS) solutions. These platforms streamline the management, settlement, and integration of stablecoins into existing financial systems, empowering businesses to innovate further.

The journey is far from over. Emerging fields like on-chain data analytics, settlement solutions, and smart contract-based AI payments promise to drive the next wave of innovation, reshaping the financial landscape.

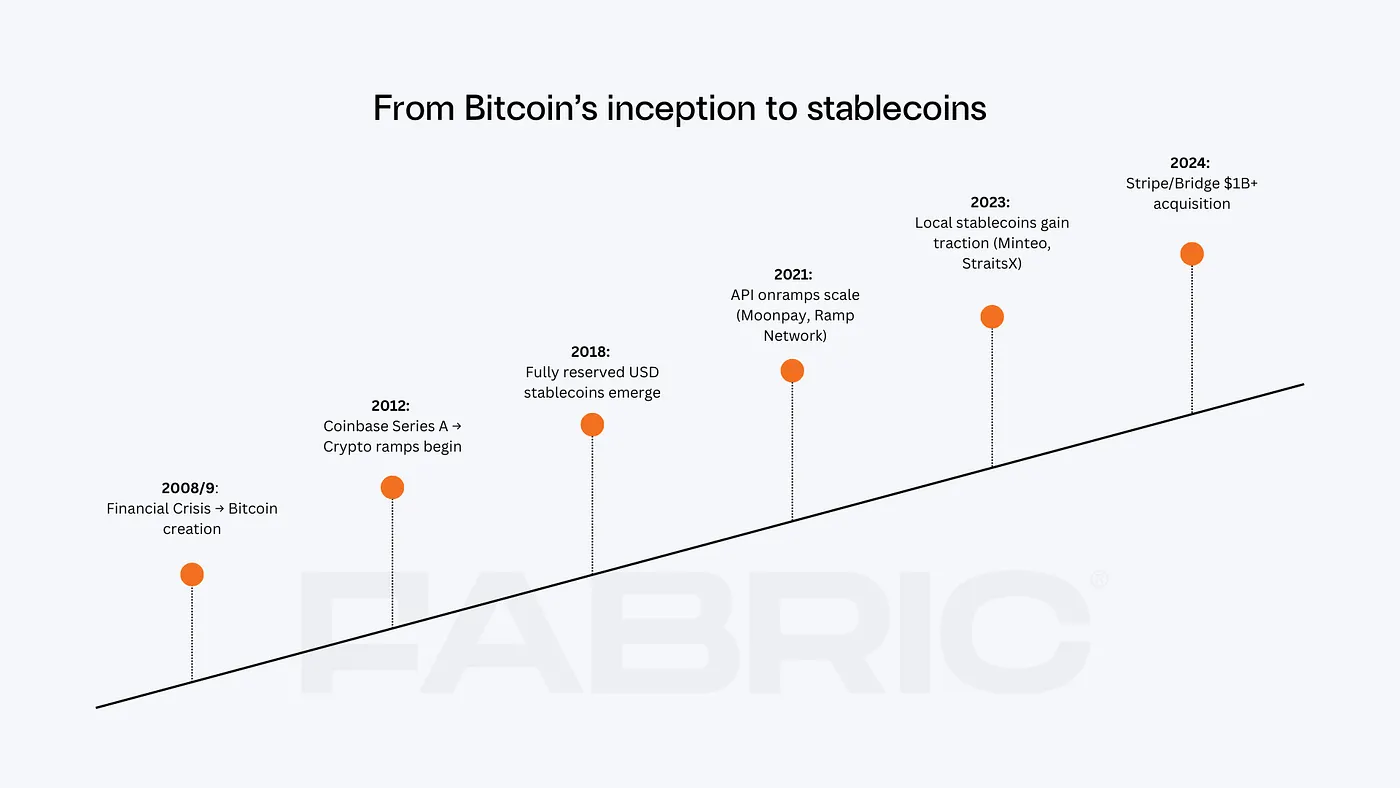

A Chronology of Events

A clear way to illustrate how far we’ve come is to look back at some key events and players:

- Regulated crypto exchanges laid the foundation for widespread adoption from 2012 onwards. Coinbase (Series A in 2012) were pioneers of ramping fiat. Local exchanges followed where crypto helped in inflation-hit regions. Yellowcard, a key player in Africa, secured its Series A in 2021, solidifying stablecoin use for remittances and USD access (via stablecoins) and Bitso did its Series A in 2016. Fabric has investments in Coinbase, Kraken, and Yellowcard.

- 2018 saw fully reserved USD stablecoins with fiat onramps emerge, with Circle pivoting from Bitcoin and Paxos raising its Series B after its pivot from a Bitcoin exchange to laying the groundwork for the stablecoin ecosystem.

- 2021 saw API onramps scale: Fiat ramps like Moonpay and Ramp Network revolutionized user onboarding via APIs vs relying on exchanges. Their Series A rounds in 2021 followed Fabric’s early investment in Ramp Network (seed round, 2018). These APIs enabled seamless integration for dApps and businesses, further simplifying access to stablecoins.

- Turbocharging dApp propositions: Some of these same dApps, such as Latin America’s Lemon Cash, emerged as retail neobanks and dollar-saving and yield-generating solutions in regions with currency instability. Lemon Cash’s Series A in 2021 demonstrated the demand for localized solutions.

- Institutional and merchant-focused crypto solutions matured. Coinbase Prime launched from their Tagomi (a Fabric investment) acquisition in 2020, targeting high-volume traders, while BVNK raised its Series A in 2022, enhancing merchant-facing tools. Fabric’s seed investment in Nilos (2022) highlighted the importance of the stablecoin use cases for merchants to cover their fiat costs or accounts payable.

- BaaS and PaaS continued evolution: Banking as a Service (BaaS) and Payments as a Service (PaaS) transitioned from Web2 fintech to crypto (Chime, the Web2 pioneer did its series A in 2016). Originally select banks such as Cross River/Lead/Banking Circle offered their own core banking solutions for this by next gen solutions have seen crypto specialists come to the forefront (Fiat Republic was backed by Fabric in 2023) with crypto compliance and on-chain analytics expertise and next gen APIs to deliver on/offramps and fiat virtual bank accounts for exchanges or other regulated players. The above model evolved to embrace non-regulated merchants who had financial money movement use cases as well as corporate customers by providing APIs, regulatory umbrella coverage and covering 3rd party payments use cases. The first wave was for B2B2C use cases (e.g. client companies who serve fiat remittance or gambling use cases). These use cases again usually involved stablecoins. Zero Hash’s Series C was in the summer of 2020 (the first round after their pivot from being an exchange). Even exchanges started to provide some of these services as well (e.g. Yellowcard). Where we are today is we are seeing the same APIs now for orchestrating payments for business use cases such as fiat invoice payments, fiat treasury sweeps or fiat payment settlement. Again these are heavily stablecoin use cases. This is where we have companies like Bridge whose Series A was in Oct 2023 and Fabric did a Seed round in Due Network in Nov 2023 and doubled down in the US in Dec 2024 with Hifi and in Asia with (to be announced) Xweave.

- Compliant mainstream stablecoins gained traction in the Eurozone, spurred by MICAR regulations and use cases of stablecoins for beyond crypto trading into payments. Players like Membrane, Monerium, and Quantoz Payments (Fabric investment in 2024) led these efforts.

- Local stablecoins: StraitsX launched their Singapore Dollar stable in 2020. Local solutions have typically been local currency stablecoins due to regulations (a perceived threat by the local banking system and regulators of the USD being used in lieu of local currency). In developing countries which do not have USDs as an inflation hedge currency of choice and where regulators have not made clear rulings (yet) there is still an increasing need for local currency stablecoins for liquidity pools as well as last mile local payment rail on/off ramps and local compliance) on the back of the surge in companies trying to solve cross-border payments and remittances on-chain (Minteo, a Fabric investment, launched theirs in 2023).

In conclusion, it takes time for regulations, technology, and real-world use cases to align. Today’s stablecoin orchestration solutions rest on earlier breakthroughs — ramps, BaaS/PaaS models, exchanges, OTC desks, unregulated stablecoins, and even Bitcoin payments. The $1bn+ Stripe/Bridge acquisition in late 2024 underscores why investors are doubling down, but Fabric has been supporting the evolution of this thesis for years, as the examples above demonstrate.

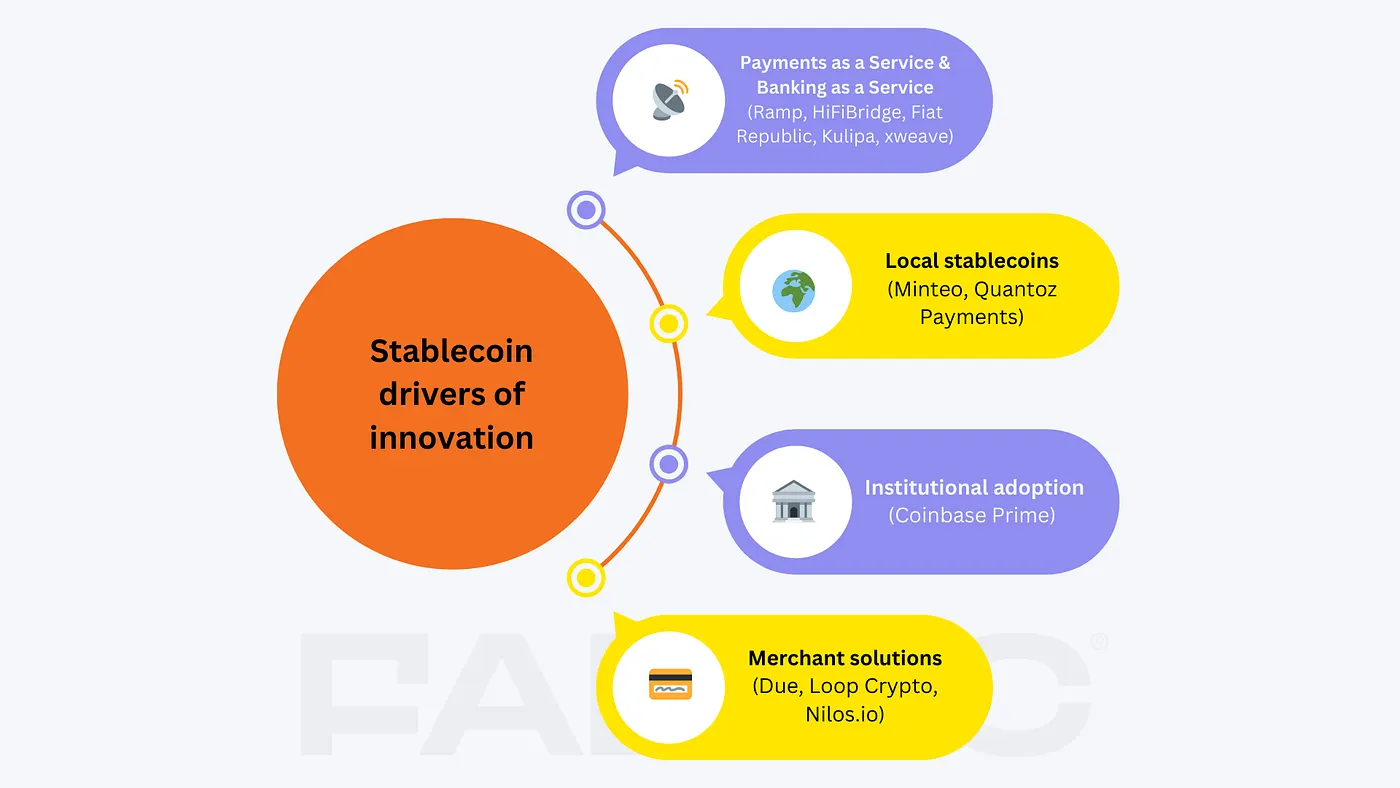

Key Drivers of Stablecoin Innovation Today (with Fabric portfolio companies as examples)

Mapping the Stablecoin Payments Value Chain

Hindsight makes it easier to identify the key investment categories, but these companies were once innovating with moving targets, pivoting as they evolved. Today, the stablecoin payments value chain can broadly be categorised as follows:

- Regulated Merchant Acceptance & API based On/Off Ramps: Developer-friendly APIs, like Stripe, simplify integration but ultimately in a price commoditising environment, it is scale of distribution and acceptance rate performance that will define future winners or targets of likely partner/acquisitions by regulated merchant acquirers.

- API based regulated BaaS & PaaS Payment Platforms managing the stablecoin movement: Whether clients are merchants, consumers or regulated entities, these are similar to trad-fi payment companies where “moats” come from volume processed, banking relationships, managing different payment methods, local payment rails, local regulation, global network reach, access to liquidity, technology uptime, and top-tier KYC/AML compliance and on-chain analytics. There will be many vertical winners depending on the use case, GTM, and corridor similar to how we see in fiat payments. To illustrate the vertical differences, Fabric has invested in Nilos (for emerging market x-border merchants), Fiat Republic (BaaS for VASPs), Fipto (for corporate payouts), HiFi (for web3/fintechs doing international to US payments) and Iron.xyz (serving PSPs and Banks for their settlement flows).

- Regulated Stablecoin Issuers: Regulations create hurdles (technical, regulatory, banking, use case GTM) to launch a scaled AUM stablecoin are very significant. See my post specifically on the challenges for launching regulated e-money tokens in Europe given regulations. There is already a trend (Minteo, Circle, Monerium, Quantoz Payments) that many of these issuers realise their future is not in purely being an AUM treasury management business but also need to provide tier 1 scalable and efficient technology and local on/off ramp rails. There is much more innovation to happen in the using stablecoins for regulated use cases outside crypto trading, such as closed loop use cases — settlement with central banks (although CBDCs are the threat here) or in capital markets, transportation, micropayments etc.

- Liquidity Providers: Such as OTC desks and exchanges (some with their own on/off ramps) where efficiency, liquidity, consumer trust, currency pair coverage and country presence are the key factors for success. Aggregation (across exchanges, OTC, p2p etc.) with API access of liquidity, especially in the longer tails, will become increasingly important to power orchestrators.

- Custody Tech Providers: Fireblocks has the scale, but niche players like Utila and Fabric-backed Narval can innovate with respectfully advanced MPC and Web3 access management tools.

- Consumer & Merchant-Focused dApps: Innovation will continue here as continues to be the case in Web2 fintech especially as players build on the infrastructure improvements solved by 3rd parties. This space delivers solutions more and more akin to Web2 consumer fintech (neobanking, trading) or corporate SaaS (treasury management, invoice solutions, accounting, CRM, ERP). Existing Web2 players are also coming such as eToro, PayPal, Revolut and Robinhood.

- Orchestrators: Payment orchestration in Web2 is a large category given the significant fragmentation in payment methods, PSPs, regulations as merchants sell more and more globally. By optimising choice and routing based on sophisticated analytics and data, costs can be reduced and payment acceptance rates are maximised. In blockchain many of these Web2 challenges are by design removed (global settlement systems, almost real time settlement, minimal costs) but fragmentation is still an issue. Solutions might be smart contract-based payment abstraction layers on top of Ethereum L2s and other chains with their own relayer infrastructure. These abstractions can manage interoperability of chains and integrations with various DEXs, bridges and liquidity networks (most payment participants will not want to manage this complexity and is analogous to the complexity Visa stepped in to solve in Web2: many currencies, settlement systems, bank issuers, and merchant fragmentation). These players can orchestrate, without touching funds, settlement, payments metadata and KYC identities between participants such as regulated partners gateways, PSPs and mobile wallets. The more exotic the end fiat currencies are the more profound is this abstraction need (e.g., Fabric-backed Xweave).

- Open Data Platforms: Enriched and open on-chain contextual transaction data unlocks new insights for credit scoring, marketing, loyalty, churn management let alone back office book keeping, taxation and accounting. With this data we can unlock new use cases just like Open Banking did for Web2. The result in Web2, with pioneers such as Plaid in the US and Tink (acquired by Visa) in Europe (both backed by my alma mater PayPal Ventures), has been today greater competition and faster development of new applications within the financial services industry. A Buy Now, Pay Later application can’t properly underwrite risk if it doesn’t know a consumer’s payment history, a revenue forecasting tool can’t provide insights if it doesn’t know how much or what exactly you sold. Fabric’s Loop Crypto investment explores these opportunities based on its own and other’s SaaS merchant gateway payments capture.

- On-Chain Settlement Rails: It is likely that general-purpose blockchains cannot meet the scale and standards of major payment networks. In addition, current solutions stablecoin payment solutions are not fully decentralised because there is a need to collect the settlement funds from the user wallet in an offramp account (for stablecoins), swap with say Circle, and then manage a settlement account (for the fiat) before the fiat funds get transferred to the merchant acquiring bank account. This centralised actor in turn needs to be regulated (e.g. E-Money License) to touch these funds. By running or partnering with an L1 or L2 that is optimised for processing and payments there is a potential to enable a self-sovereign banking experience. These solutions effectively will create an entirely new end-to-end acceptance and settlement process on-chain (bypassing traditional networks like Visa or Mastercard or Banks) so that merchants receive faster payments with reduced fees. Fabric’s investment in Codex.is aims to redefine payment settlement processes on-chain, as do companies such as Stables. Blockchain innovators could cut into the financial services card scheme fee “racket” by allowing merchants to charge lower fees for users of its on-chain settled cards through discounts to consumers. They could circumvent the scheme fees and could send merchants rewards (to pass on to consumers) for charge activities using their cards, from some of the interest received from the fiat that back the stablecoins used. Fabric’s investment in Kulipa in Jan 2024 was done with this in mind. Extending this thesis of on chain settlement brings us to emerging stealth solutions, founded by friends of Fabric, enabling on chain treasury/FX for multi-jurisdictional Corporates or PSPs (Velocity) and solutions powering multi-jurisdictional on chain blockchain-based current account banking (ValoX).

- Smart Contract & AI-Powered Payments: The big win in blockchain based payments will actually be less about the current focus on efficiency and costs of settlement and instead arise from leveraging the programmability of smart contracts. Imagine payments with embedded rules to deliver built-in controls on where and how funds can be sent e.g. solving the complexity of middle/back office for bond settlements or how payments might be frozen, e.g. adhering to regulatory requirements. Fabric-backed Superfluid Finance and idOS Network drive this shift toward autonomous and modular composable finance. Smart contracts can carry out specific “if-then” logic transactions based on predefined terms and conditions connected immutably to specific characteristics such as purchase behaviour, delivery and loyalty and even AI-powered algorithms embedded in them, enabling autonomous agents to negotiate and transact between themselves.

New players in categories like Merchant Acceptance (point 1 above) and Liquidity Providers (4) are unlikely, with consolidation likely taking center stage. Founders building new differentiated projects in Custody Tech (5) offer exciting potential for breakthrough innovation and we would love to learn about them. Consumer dApps (6) will likely face stiff competition from established Web2 giants but a true on/cross chain self custody neobank is needed. Stablecoin Issuers (3) will remain dominated by incumbents (or incumbent backed startups) for crypto liquidity, though localized and closed-loop use cases are set to emerge. The BaaS/PaaS (2) and Orchestrators (7) also stand out as a greenfield volume growth opportunity but also one where the traditional world will need to partner (as customers, acquirers and founding teams combining both blockchain and trad-fi skills) with the blockchain native teams to bring down the structural costs of fiat-based trade. As the real world use cases expand (into treasury management, capital markets, banking, e-commerce, payroll, and subscriptions), the TAM will get too large to ignore and thus this remains an area of focus for Fabric. It already was too big to ignore for Stripe when it acquired Bridge for >2bn$.

To end on a call for action for where the puck is heading — categories like Open contextual payment Data (8), Settlement Rails on-chain (9), and AI-Agent Payments (10) are where we, at Fabric, see some of the most ambitious and capable founding teams focusing for the next evolution of blockchain payments. Fabric has published its latest Web3 thesis specifically addressing the intersection of Blockchain, Open Data and AI which includes a vision of open, modular, programmable, and automated payments. The holy grail is that every piece of software in the future will be somehow agentic, replacing much of today’s software. A natural evolution of autonomous agents is enabling them to negotiate and complete their tasks with payments. We are not alone: The recent announcement by Stripe to create a payment SDK for AI agents joins similar moves by Coinbase, Circle, and soon OpenAI and Perplexity, signaling a growing wave of interest in combining AI agents with payments and the policy frameworks that govern the transaction. If you are one of these founders, please reach out as we would love to learn more and compare notes.

• • • • •

For more information on Fabric’s portfolio, opportunities and our investment thesis please visit our website and follow us on Twitter, LinkedIn, Farcaster & Orb.