Evaluating Long-Term, Non-Speculative Value

Co-written with Richard Muirhead, in collaboration with Anastasiya Belyaeva & Julien Thévenard.

As often as projects have claimed that their token will accrue value proportionately to the usage of the network, we’ve heard investors claim that by the Law of MV=PQ, tokens will have no value as a result of high velocity. Both of these are inaccurate simplifications and generalisations.

As a brief refresher on the argument against value accruing to tokens:

Expected high velocity — The more successful a network, the more often its token will exchange hands in the form of payments.

No incentives to hold — Additionally, since in the future swapping from one token to another token will happen frictionlessly in the background, users will hold stablecoins or Store of Value (SoV) tokens and exchange these for the payment token ‘just in time’. In the absence of any other incentives for users to hold any amount of the native payment token, they are likely to hold none.

No need for token (can be forked out) — The payment token might even be swapped out in a new fork of the network as it only adds friction for users who hold stablecoins or SoV.

Using MV=PQ to value tokens — As a result, a transacting user will hold the payment token as briefly as possible and the velocity of that token will increase heavily. Following the equation of exchange MV=PQ, in a network’s ultimate equilibrium state, as the real value of the network PQ stabilises, the high aggregate velocity axiomatically indicates a falling value of M and hence very little value accrual in the native payment token itself.

In the case described above, where “tokens” are characterised as predominantly or exclusively payment enablers, we’re broadly aligned with John Pfeffer’s thoughts in the long run and absolutely recommend reading his excellent analysis on the subject which has dominated the narrative around payment tokens for the past 6 months: An (Institutional) Investor’s Take on Cryptoassets.

• • • • •

It is however worth noting a few further points concerning the purist application of Fisher’s century-old and much debated equation of exchange. MV=PQ is a seductively simple economic identity, but its applicability to the crypto market is far from validated: the directionality of cause and effect; the assumed equilibrium state; the impact of speculative transactions; the composition of aggregate velocity; and the effect of distribution of holdings have not yet been sufficiently well analysed.

- Cause and effect: Historically, it is principally PQ and M that have been the drivers of the equation — V was included as a multiplier to make the equation work (see Friedman — “[V has] generally been calculated as the number having the property that it renders the equation correct”). More pragmatically, V is a result of the equation, solving for how many times each unit of currency needs to change hands at a price point (accounted in M) to equate to the output of the economy (PQ).

- Equilibrium: It assumes near perfect information and market behaviour and that supply and demand for the means of payment will lead to an equilibrium that has never and is unlikely to ever be observed in reality.

- Speculative transactions: As Chris Burniske points out in his original writings, a significant number of transactions will not be linked to “an exchange of value for the digital resource of the network, but instead a means of speculation, which is excluded from GDP metrics”. These transactions should be ignored when thinking of V.

- Aggregate velocity: As Chris further illustrated, aggregate velocity is a weighted average of velocities of a cryptoasset in different use cases: e.g. transactional velocity and holding/staking velocity of a single token. As a result, in a case where a large proportion of tokens are used for investment or cautionary/hedging purposes, aggregate velocity can be decreasing while transactional velocity is increasing.

- Distribution of holdings: Quantity Theory of Money assumes a high distribution of holdings, which is rarely observed in early stage decentralised networks. As Prof. Michael Mainelli suggests that “the economic usefulness of a [cryptoasset] depends to a large extent on how evenly distributed it is. If a handful of people own nearly all of it, then, even if there are many people with non-zero holdings, its usefulness will be limited”. Instead, one might want to look at “d(H)MV=d(A)PQ where d(H) is a distribution of holdings and d(A) is a distribution of activity”.

• • • • •

Nonetheless, this post is focused on a bigger area of opportunity that is sidelined by the above debate. As Jack du Rose points out, the term utility token is currently often misapplied to all tokens that are not purely security tokens. Whether it’s an attempt to hide under a blanket statement to avoid securities regulation or simply the product of imprecise labelling, the reality is that the subsets of tokens that are being engineered are far broader than security and payment tokens.

Tokens can be engineered to serve a greater purpose than payments and fundraising: designed properly, tokens represent the ownership of scarce digital resources and coordinate the actors in a given network. As a result, such tokens drive the incentives for both existing and prospective network keepers to competitively provide good work as suppliers; govern in favour of the network; participate productively as users; and collectively provide the security of the network against sybil attacks.

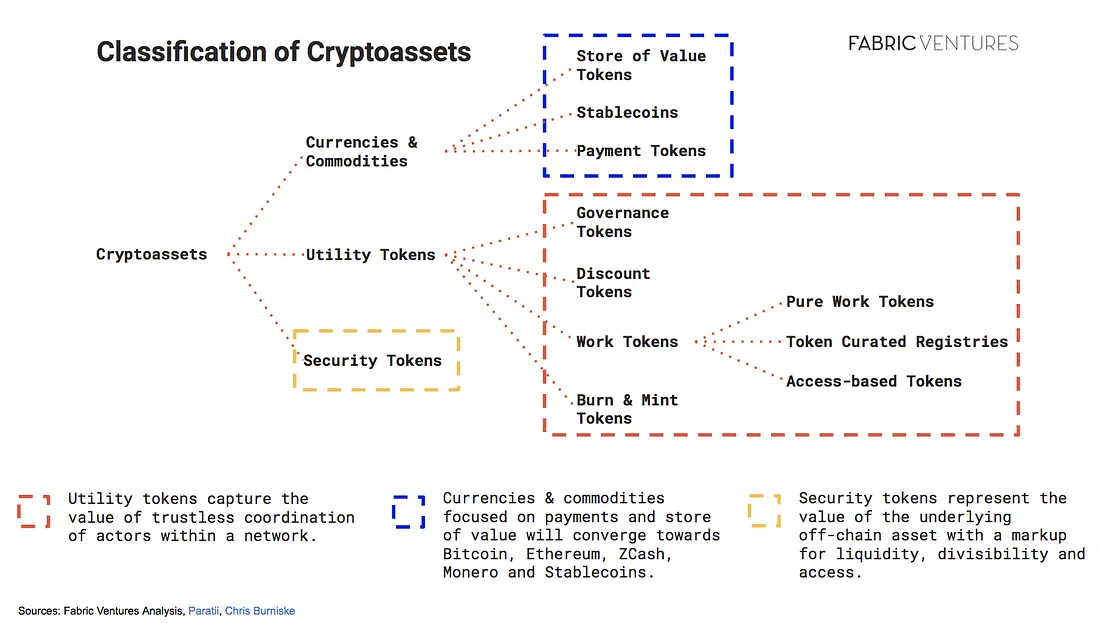

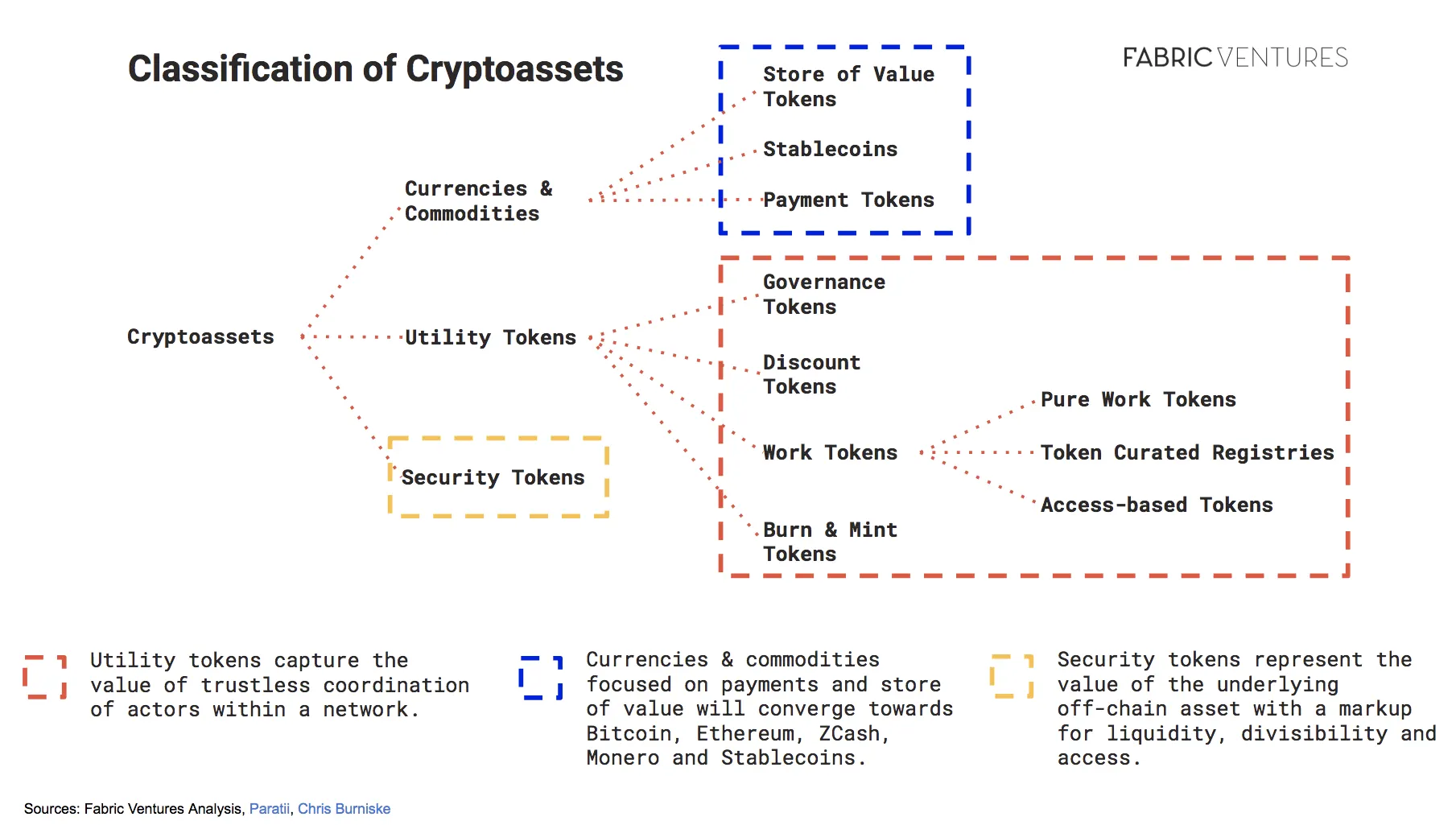

Thus, bearing in mind that a cryptoasset might have several characteristics and a network might contain more than a single cryptoassets, we look at the classification of the characteristics of cryptoassets as follows:

- Currencies & Commodities: Tokens that serve as means of payment, store of value, or unit of account.

- Utility Tokens: Tokens that act as an access, coordination & security mechanism inside a network.

- Security Tokens: Tokens that represent existing off-chain securities (from equity to real estate).

This subgroup of Utility Tokens are core to our investment thesis. These are tokens that implement a skin-in-the-game mechanism for communities to coordinate around a network. Individual users and other entities need to stake/hold them in order to:

- Provide profitable future work to the network

- Influence information & content in the network

- Participate in the governance of the network

- Build & maintain a data footprint for reputation, credit or other purposes

- Gain access to goods and services provided in the network

• • • • •

To take a practical example, let’s look at a hypothetical pure Work Token (in its current state of the art) and how it relates to the core criticisms put out against payment tokens:

a) Expected high velocity

b) No incentives to hold

c) No need for token (can be forked out)

d) Using MV=PQ to value tokens

a) Velocity

Work tokens generally act as a “licence”. Users or other entities controlling a given number of nodes must acquire and stake these tokens to perform a service in the network.

The network commonly then chooses workers on a probabilistic basis, where the odds of being chosen are proportional to the number of staked tokens. These staked tokens also act as a security deposit, which can be taken from the node in cases of misbehaviour.

Instead of acting as a currency for exchange of value, work tokens grants the right to capture future value from the network, much like a taxi medallion allows a driver to earn a living in New York City. Contrary to the US Dollars used to settle each individual trip, the velocity of such tokens will be as negligible as that of a taxi medallion.

→ Work tokens will primarily be owned by entities providing work to the network, these will be staked, and therefore held, for as long as these entities desire to participate in the network. The velocity signature of such a token will clearly be lower than that of a purely transactional one.

b) Incentives to hold

While users of a payment token can expect to store their assets in a stablecoin or a SoV and quickly switch into a payment token as it’s needed, keepers in a work token network cannot buy their token after the fact — they need to continuously hold & stake the token in order to benefit from it.

Additionally, within these digital economies, there are frequently data level network effects that result from increased & consistent staking e.g. reputation data is deepened; credit scores become more accurate; and ‘back catalogue’ of content is increased. These network effects reinforce the “relative value” of staked tokens to their staker, and decrease their likelihood of transacting them (e.g. losing the reputation they’ve built up over a period of time of providing good work).

→ Keepers have even stronger incentives to hold over time.

c) Need for the token

On the note of forking, we don’t believe this to be as easy as often claimed. From a technical perspective — forking a network and meaningfully differentiating it in terms of features is non-trivial. But perhaps more importantly, we’re convinced that teams matter, that communities matter, and that brands matter & strengthen network effects.

From a “hodler’s” perspective, a fork is generally easy & effortless to adopt. However from an active user’s perspective, a fork creates complications around ecosystem integrations, development updates, and technical tools. Furthermore, the team and community of early adopters will have skin-in-the-game with the tokens they’ve designed and will not move on so easily. Instead they will keep building exciting new features in order to maintain the networks in a dynamic state. As a result, the networks never reach the “final steady state equilibrium” where such static forking could be possible.

But more importantly, work tokens are needed by the network, not as means of payment, but as instruments for coordination and security of the network. When looking at the cost of a potential attack, these work tokens make it extremely expensive and difficult for an attacker to succeed. Their very specialisation and scarcity delivers greater value the more in demand or under pressure the network become. As an illustration, consider the case of a 51% attack where a bad actor is attacking a network that has $50m staked.

- Buying $26m worth of native tokens will be very difficult: as this represents a large part of the outstanding tokens, each additional buy will significantly push up the market price. In fact, it’s even highly likely that total market liquidity would be insufficient to acquire enough tokens to perform a 51% attack. These prohibitively high attack costs combined with the expected loss of value in native tokens following the attack make native tokens an efficient security mechanism.

- The same attack would be significantly simpler and cheaper if the staking was performed in BTC or ETH. Buying $26m of BTC or ETH would barely move the market price, and additionally the attacker would not stand to lose any value in their staked BTC or ETH as their price is uncorrelated to the value of the network they are attacking.

Work tokens are effectively the only thing that puts skin-in-the-game for the keepers of the network. Just as Bitcoin miners have significant costs locked up in ASICs which would lose significant value if they were to attack the Bitcoin Blockchain, keepers of networks have costs locked up in staked tokens which would lose significant value if they were to attack the network.

→ The native token is therefore a necessity to both trustlessly coordinate actors & secure the network.

d) Valuation mechanisms

The starting point of an analysis of the value of such work tokens would not consider them as a medium of exchange, unit of account or a store of value, which they primarily are not. As such, the application of MV=PQ would be an incorrectly retrofitted model. Instead, such tokens should be valued based of the future expected cash flows attributable to workers in the network, which can be modelled out based on assumptions on pricing and usage of the network. This can be achieved by traditional Discounted Cash Flow (DCF) analyses or even by looking at valuation techniques for Taxi Medallions.

If employing a DCF model, one would calculate the expected future cash flows of all keepers (“mining” rewards & service payments), which, assuming a constant service rate, will increase proportionally to the usage of the network. An equilibrium valuation would be found at a point where the net present value of the keepers’ cash flows marginally outsize the cost of staked capital & running costs for a threshold internal rate of return.

→ MV=PQ is not relevant to work tokens — instead one would use a future revenue based analysis (DCF or similar).

• • • • •

Conclusion:

To simplify the discussion we have focused on a work token, but there is also utility to tokens with governance, discount, curation and other critical characteristics. Going forward, we’d like to encourage the investment community to clearly differentiate between a simple payment token and the complex cryptoeconomic designs which have been pushed forward by the likes of Ocean Protocol, Augur and Keep Network. In the future, we foresee that in numerous networks the native token will not even be used for payments between parties — the role of payments will be instead usefully delegated to stablecoins or SoV tokens. For valuing such networks, the application of MV=PQ seems secondary, and we should instead look at the revenue generating opportunities for keepers coordinated with the benefits to positively participating users.

We agree that many current tokens are simply network-native payment tokens, and these most probably will not accrue much value over the long term. However, tokens are ‘just software’, and as such can be programmed with infinitely sophisticated logic — and incentive mechanisms. To the extent that balanced economic incentives exist in the ‘real’ world, they can be built into cryptoassets. We certainly believe that properly engineered cryptoeconomic incentive and participation systems will accrue value, and we see the opportunity for enduringly valuable and impactful networks as a result. Indeed, it is in the interests of early developers and investors to iterate tokens and their network economics to precisely this end.

• • • • •

With thanks to Jess Houlgrave, Chris Burniske, Trent McConaghy, Lanre Jonathan Ige & Joe Urgo for the insightful comments and a special thank you to David Fauchier for pushing us to rethink the flow.

• • • • •